VA Loan Benefits 2025: Maximizing Zero-Down Payment Opportunity

Breaking news indicates that VA Loan Benefits 2025 are being refined to further empower eligible individuals with significant zero-down payment opportunities, streamlining the path to homeownership for veterans and service members.

In a developing story impacting military families nationwide, discussions and legislative movements are currently underway that point towards enhanced VA Loan Benefits 2025: Maximizing Your Zero-Down Payment Opportunity. These potential changes are designed to make homeownership more accessible and affordable for our nation’s veterans and active-duty service members, offering a vital pathway in an ever-evolving housing market.

Understanding the Core of VA Loan Benefits

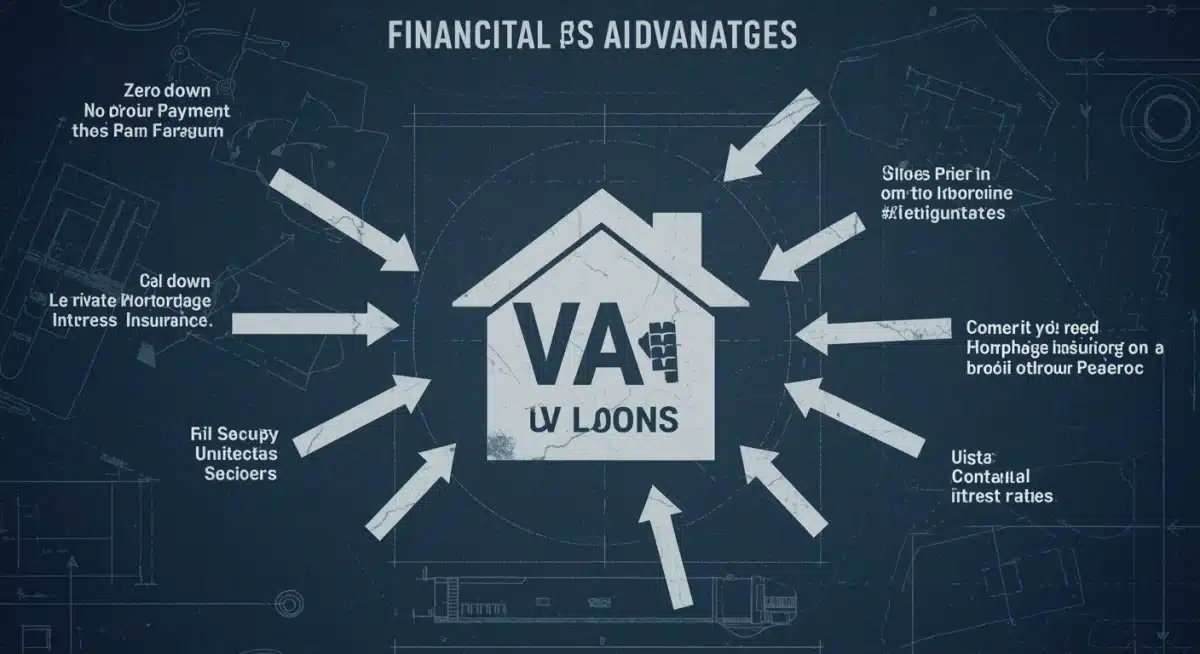

The VA Loan Program, backed by the U.S. Department of Veterans Affairs, stands as a cornerstone for military personnel seeking homeownership. Unlike conventional mortgages, VA loans offer unique advantages, primarily the ability to purchase a home with no down payment. This critical benefit significantly reduces the initial financial hurdle for many eligible individuals, allowing them to enter the housing market with greater ease. As we approach 2025, the program continues to adapt to economic realities and the needs of its beneficiaries.

The program’s success is rooted in its objective to honor service by providing tangible support. Eligibility typically extends to veterans, active-duty service members, and certain surviving spouses. Understanding these foundational elements is crucial before delving into the specifics of upcoming changes. The VA guarantees a portion of the loan, which encourages private lenders to offer more favorable terms, including competitive interest rates and no requirement for private mortgage insurance (PMI).

Eligibility Criteria for VA Loans

To qualify for a VA loan, applicants must meet specific service requirements set by the Department of Veterans Affairs. These criteria ensure that the benefits are directed to those who have honorably served our country. The Certificate of Eligibility (COE) is the key document that confirms a service member’s eligibility.

- Service Duration: Generally, 90 consecutive days of active service during wartime, or 181 days of active service during peacetime.

- National Guard/Reserve: Six years of service in the National Guard or Reserves.

- Spouses: Certain surviving spouses of veterans who died in service or from a service-connected disability.

- Discharge Type: Honorable discharge is typically required for veterans.

Zero-Down Payment: A Game Changer in 2025

The zero-down payment feature remains the most attractive aspect of VA loans, particularly as housing costs continue to rise. For 2025, this benefit is expected to be maintained, ensuring that eligible borrowers can purchase homes without the significant upfront capital typically required for conventional mortgages. This is especially impactful for younger service members or those who have not had the opportunity to build substantial savings.

The ability to secure a home without a down payment directly addresses a major barrier to entry in competitive housing markets. This benefit, combined with the absence of PMI, allows borrowers to allocate more of their financial resources towards other aspects of homeownership, such as renovations or emergency savings. The VA’s commitment to this benefit underscores its dedication to supporting the financial well-being of military families.

Impact on First-Time Homebuyers

For many first-time homebuyers within the military community, the zero-down payment option is transformative. It allows them to transition from renting to owning much sooner than would be possible otherwise. This accelerates wealth building through home equity and provides stability for families who often face frequent relocations.

The financial relief from not needing a down payment can also alleviate stress during a PCS (Permanent Change of Station) move, enabling service members to secure housing quickly and efficiently. This flexibility is invaluable, especially in high-cost-of-living areas where down payments can easily run into tens of thousands of dollars.

Navigating Funding Fees and Loan Limits

While VA loans offer zero down payment, they do come with a VA funding fee. This fee helps offset the cost of the program to taxpayers and ensures its continued availability. However, certain veterans, particularly those receiving VA disability compensation, may be exempt from this fee. Understanding these nuances is crucial for maximizing the overall financial benefit of a VA loan.

For 2025, current discussions suggest a continued focus on ensuring the funding fee structure remains equitable and supports the program’s sustainability. Additionally, for eligible borrowers with full entitlement, there are no loan limits, meaning they can borrow as much as a lender is willing to offer without a down payment, provided they meet the lender’s credit and income requirements. This is a significant advantage over conventional loans, which often have strict limits on loan amounts without a substantial down payment.

Exemptions and Waivers for the Funding Fee

Knowing if you qualify for a funding fee exemption can save thousands of dollars. The primary exemption applies to veterans receiving VA compensation for a service-connected disability. Other exemptions include:

- Veterans who would be entitled to receive compensation for a service-connected disability if they did not receive retirement or active duty pay.

- Service members on active duty who have been awarded the Purple Heart.

- Surviving spouses of veterans who died in service or from a service-connected disability.

Competitive Interest Rates and No PMI

Another significant advantage of VA loans for 2025 is their typically competitive interest rates, often lower than conventional rates. This, combined with the absence of private mortgage insurance (PMI), translates into substantial long-term savings for homeowners. PMI is usually required for conventional loans when the down payment is less than 20%, adding a monthly cost that VA loan borrowers avoid entirely.

The elimination of PMI can reduce monthly mortgage payments by hundreds of dollars, making homeownership more affordable over the life of the loan. This benefit is a direct result of the VA’s guarantee to lenders, which mitigates risk and allows them to offer more favorable terms to military borrowers. This financial relief is a key component of maximizing the overall value of the VA loan program.

Long-Term Financial Advantages

The cumulative savings from competitive interest rates and no PMI can be substantial. Over a 30-year mortgage, these savings can amount to tens of thousands of dollars, freeing up capital for other investments or family needs. This long-term financial stability is a core objective of the VA loan program, empowering military families to build equity and secure their financial future.

Moreover, the absence of PMI means that borrowers are not paying for insurance that primarily benefits the lender. Instead, every dollar paid goes directly towards the principal and interest of their home, accelerating equity growth and overall financial health. This makes the VA loan an exceptionally powerful tool for long-term financial planning.

Refinancing Options: IRRRL and Cash-Out

VA loans also offer robust refinancing options, including the Interest Rate Reduction Refinance Loan (IRRRL), often called a VA Streamline Refinance, and the VA Cash-Out Refinance. These options provide flexibility for homeowners to adjust their mortgage terms or access their home equity, further maximizing the benefits of their initial VA loan.

The IRRRL allows borrowers to refinance an existing VA loan to a lower interest rate or convert an adjustable-rate mortgage (ARM) to a fixed-rate mortgage, often with minimal paperwork and no appraisal required. The Cash-Out Refinance, on the other hand, enables borrowers to take cash out of their home equity for various needs, such as home improvements, debt consolidation, or other financial goals, even if the original loan was not a VA loan.

Strategic Use of Refinancing

Strategically utilizing VA refinancing options can significantly enhance a veteran’s financial position. An IRRRL can lead to lower monthly payments and substantial savings over the life of the loan, especially if market rates drop. A Cash-Out Refinance offers a powerful way to leverage home equity, providing financial liquidity when needed.

- IRRRL: Simplifies refinancing, often without an appraisal or income verification, to secure better terms.

- Cash-Out Refinance: Allows access to home equity, even if the original loan was not a VA loan, up to 100% loan-to-value in some cases.

- Flexibility: Provides options to adapt to changing financial circumstances or market conditions.

Preparing for VA Loan Application in 2025

As 2025 approaches, prospective VA loan applicants should begin preparing their documentation and understanding the application process. While the benefits remain substantial, a smooth application requires careful attention to detail. Gathering your Certificate of Eligibility (COE), understanding your credit score, and pre-qualifying with a VA-approved lender are essential first steps.

The housing market can be dynamic, and being prepared ensures that you can act quickly when the right opportunity arises. Staying informed about any legislative updates or policy changes related to VA Loan Benefits 2025 will also be crucial. Consulting with a lender specializing in VA loans can provide personalized guidance and streamline the entire process, leading to a successful home purchase.

Key Steps for a Smooth Application

Proactive preparation can make a significant difference in the VA loan application journey. Starting early with essential documentation and financial assessments is highly recommended.

- Obtain Your COE: This is the foundational document proving your eligibility.

- Check Your Credit: Ensure your credit score is in good standing, as lenders will review this.

- Pre-Approval: Get pre-approved by a VA-approved lender to understand your borrowing power and demonstrate seriousness to sellers.

- Research Lenders: Compare offers from multiple VA-approved lenders to find the best terms and rates.

| Key Point | Brief Description |

|---|---|

| Zero Down Payment | Allows eligible service members and veterans to purchase homes without an initial down payment, easing financial burden. |

| No Private Mortgage Insurance (PMI) | Eliminates monthly PMI costs, significantly reducing overall mortgage payments and increasing savings. |

| Competitive Interest Rates | VA loans typically offer lower interest rates compared to conventional loans, leading to long-term financial benefits. |

| Funding Fee Exemptions | Veterans with service-connected disabilities and certain others may be exempt from the VA funding fee, reducing closing costs. |

Frequently Asked Questions About VA Loan Benefits 2025

The main advantages include zero down payment, no private mortgage insurance (PMI), competitive interest rates, and reduced closing costs. These benefits are designed to make homeownership more affordable and accessible for eligible service members, veterans, and their families, reflecting ongoing federal support for military personnel.

Eligibility typically extends to veterans, active-duty service members, and certain surviving spouses. Specific service requirements, such as minimum active service duration during wartime or peacetime, or years of service in the National Guard or Reserves, must be met. A Certificate of Eligibility (COE) confirms these qualifications.

Yes, the zero-down payment feature is expected to remain a core benefit of VA loans in 2025. This critical advantage allows eligible borrowers to purchase homes without needing a substantial upfront cash payment, significantly lowering the barrier to entry for homeownership, especially in fluctuating housing markets.

The VA funding fee is a one-time payment that helps keep the VA loan program running. It can be waived for veterans receiving VA compensation for a service-connected disability, those who would be entitled to it but receive retirement pay, service members awarded the Purple Heart, and certain surviving spouses.

VA loan interest rates are typically competitive, often lower than conventional rates, due to the VA’s guarantee to lenders. This, combined with the absence of private mortgage insurance, results in lower monthly payments and significant long-term savings for eligible borrowers, making VA loans a highly attractive financing option.

What Happens Next

As 2025 approaches, military families and housing professionals should closely monitor legislative developments and official announcements from the Department of Veterans Affairs. Any adjustments to funding fees, eligibility criteria, or program enhancements will directly impact how service members and veterans can leverage their home loan benefits. Keeping abreast of these changes is essential for maximizing the significant zero-down payment opportunity that VA loans present. We will continue to report on these crucial updates as they emerge, providing immediate context and analysis for our readers.